18-06-2024

7 min read

Atom bank records best year since launch

Atom bank records best year since launch

- Atom bank has hit a milestone of full profitability, both before and after tax, with operating profit rising to £27m, up from £4m last year

- This progress has been driven by a 39% increase in lending, providing customers with competitive rates combined with market leading service

- Bank maintains outstanding customer service with a 5* ratings across Trustpilot, iOS and Android and highest Net Promoter Score (NPS) in its history

- Atom’s lean, low-cost business model is designed to create long-term sustainable growth and profitability, and challenges the status quo in UK banking

Atom bank, the UK’s first app-based bank, has today announced its strongest ever financial results, driven by a significant increase in lending while keeping costs exceptionally low. Operating profit grew to £27m, a 600% increase on last year, with costs up just 4%, demonstrating the success of its efficient, sustainable and scalable business model.

Atom’s low-cost and scalable model

Atom delivered its first year of operating profit in FY23, and has continued to build on this. Alongside the significant growth in operating profit, the Bank has now delivered its first full year of profit both before and after tax.

Atom raised £100m from existing investors in November last year, and the additional capital has been used to accelerate balance sheet growth and to further scale the business. This raise, against a very challenging market backdrop, was a hugely significant vote of confidence in Atom’s business model.

Despite this growth, administrative and general costs have increased by just 4%. This growth has not come at the expense of customers either, and Atom bank has maintained an outstanding customer service reputation, with a 5* ratings across Trustpilot, iOS and Android, whilst delivering a customer Net Promoter Score (NPS) of 88+, the highest in Atom’s history.

With a disparity in capital requirements between dominant incumbents and challenger banks still impeding growth and competition, the digital lender remains focused on delivering its IRB programme as Atom believes it to be the best route to address the competition imbalance that exists today in UK banking.

Lending drives growth

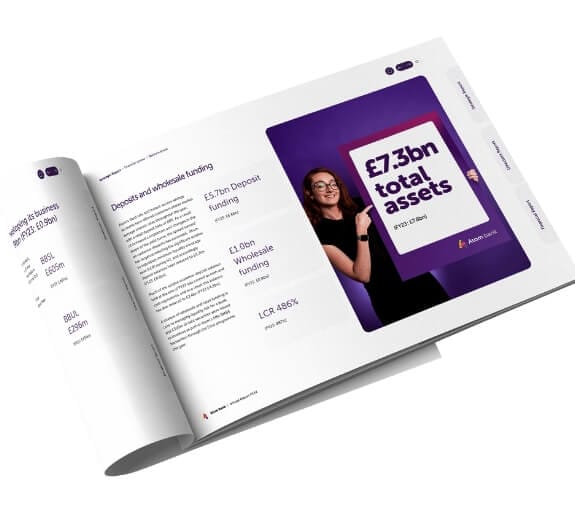

Strong loan book and revenue growth saw a 31% increase in Atom’s net interest income, to £100m, while net interest margin remained strong at 2.8% (FY23: 2.8%). The size of Atom’s loan book increased significantly by 39% to £4.1bn. A key element was the growth in residential mortgage balances to £3.2bn, an increase of 55%, as Atom navigated a difficult market to help more people achieve their dream of buying their own home. The digital lender delivered residential mortgage completions of almost £1.6bn – a 20% increase, in a market that contracted by 25%. Despite the growth in mortgages, Atom maintains very close control over credit quality, ending the year with just 0.3% of residential loans in arrears or subject to forbearance measures. This figure is 0.7% across the whole portfolio, including business lending.

This growth was achieved while maintaining market leading levels of service, and a median application to offer time of just four days (industry average 11 days) across the residential mortgage range up to 95% LTV. Atom has also focused on supporting customers with less than perfect credit, who have struggled to secure a mortgage with high street lenders in the current climate, through its tailored Near Prime mortgage offering.

The bank has also seen significant growth in commercial mortgages, ending the year with balances of more than £600m, an increase of 19%. This includes completions of over £200m, and a retention rate of maturing loans of 43% (FY23: 5%). During the year, Atom further automated commercial mortgage loan origination, making more than 100 transformative changes to its broker portal and underwriting process. Over the year, this reduced the time from loan application to securing an Agreement in Principle by 94%, down to just one working day by the end of March 23.

Better value for savers

Atom continues to focus on driving value into the UK savings market, and its fixed rate and instant access savings products have offered customers highly competitive rates throughout the year. With an interest rate deposit beta of 88%, the bank has comfortably outperformed the major high street lenders and building societies when it comes to offering savings customers a better deal.

Impact on environment and community

The Bank remains committed to making a positive impact on the environment and its local community. It has a long-term target of being carbon positive by 2035. Significant progress was made in FY24, with a 12% reduction in operational carbon emissions per full time employee (FTE) achieved, lowering carbon emissions per FTE to 1.31t Co2e.

The Bank has continued to deploy its social investment strategy in the North East, and has undertaken new initiatives including funding two new Women in Technology scholarships at Durham University, and launching the Atom Futures Fund, providing financial support to year 13 students growing up in care or from low-income backgrounds in County Durham who apply to a Russell Group University.

Mark Mullen, Chief Executive Officer at Atom, said:

“This has been our best year yet at Atom bank. We have achieved profitability across all measures, grown our loan book significantly, maintained robust credit quality, avoided fraud losses altogether, kept our costs tightly controlled and enhanced our already industry leading customer experience metrics.

“We begin the new year with tailwinds in the form of strong asset pipelines, excellent technology, a highly engaged team, supportive investors and an enviable reputation with customers. Beyond the confines of banking, we have exciting plans to further reduce our impact on the planet and to create even more opportunities in our local community.

“UK banking remains dominated by players with low growth, high costs and indifferent customer service. We remain entirely focused on serving the needs of borrowers and savers, without the soaring costs and operational complexity of transactional banking products like current accounts. Ultimately, this is the only way to disrupt the status quo.”

ENDS

Notes to editors

For more details journalists can contact:

For Lansons

Ed Shelley, eds@lansons.com 07825 427522

Sorcha Hornett, sorchah@lansons.com 07712 805191

For Atom

Robbie Steel, robbie.steel@atombank.co.uk 07538 775 701

About Atom bank

Atom bank is the UK’s first app-based bank, on a mission to make the experience of borrowing and saving faster, simpler and better value than anyone else.

The bank launched operations in April 2016, and offers award-winning mortgages and savings through its app, alongside commercial mortgages for small and medium-sized enterprises.

Based in the North East of England with a team of over 500 people, Atom is here to change banking for the good, for the better, and for everyone. This means focusing on customers’ needs, delivering better value than the incumbents, providing an exceptional app-based experience and offering award-winning customer support via phone, chat, email and social channels. The bank has some of the best customer service credentials in the UK, having achieved 5-star ratings on both the iOS and Android App Stores, and on Trustpilot, whilst consistently delivering Net Promoter Scores (NPS) in the high 80s.

Based in Durham, Atom is an engaged and active member of the North East Community. In 2022 Atom signed a five-year Memorandum of Understanding with Durham University to progress key research and diversity initiatives. The region has one of the highest levels of youth unemployment in the UK and Atom is passionate about addressing the critical digital skills gap and helping develop young people and other groups that are under-represented within the industry.

As of November 2021, all employees enjoy a four-day working week, after Atom became the largest company - and only bank - in Britain to introduce the policy, with no reduction in salary.

The Atom executive team are highly experienced, having built and run some of the most well-respected banks in the UK. CEO Mark Mullen has 30 years’ experience in the sector and was previously CEO at the multi-award-winning telephone and internet bank first direct. The team is supported by a strong non-exec board, chaired by Lee Rochford.